The compounding benefits from reinvesting dividends

.

If you invest either directly or indirectly in the biggest companies listed on the Australian share market, there’s a reasonable chance you will soon be receiving some income distributions.

In tandem with announcing their latest half- or full-year financial results to 31 December 2023, 83% of the 200 biggest companies listed on the Australian Securities Exchange (ASX) have declared dividends per share that they will pay out to their shareholders over the next month or so.

Shareholders also include the exchange traded funds (ETFs) that are direct investors in Australian-listed companies. For example, Australia’s largest ETF, the Australian Shares Index ETF (VAS) has shareholdings in the top 300 companies on the ASX and tracks the S&P/ASX 300 Index.

The ASX company dividends received by ETFs such as VAS will be aggregated and then passed through to individual ETF unitholders as income distributions.

How much ETF unitholders are paid depends on the total value of the company dividends received by the ETF and then on the number of individual ETF units held at the time a fund’s distribution payment amount is announced.

The case for reinvesting

When it comes to company income distributions, ETF investors typically have the option of taking their distributions as cash payments or reinvesting the equivalent value of their cash distributions back into additional ETF units.

ETF income distributions are generally made on a quarterly basis, but some ETFs make more frequent income payments.

Taking the cash option often relates to an individual’s income needs. However, the alternative strategy of using income distributions to purchase additional ETF units can significantly compound both capital growth and income returns over time.

Another key advantage of reinvesting income distributions is that there are no additional brokerage fees involved when ETF units are added to an existing holding, meaning lower investment costs and higher returns.

VAS case study

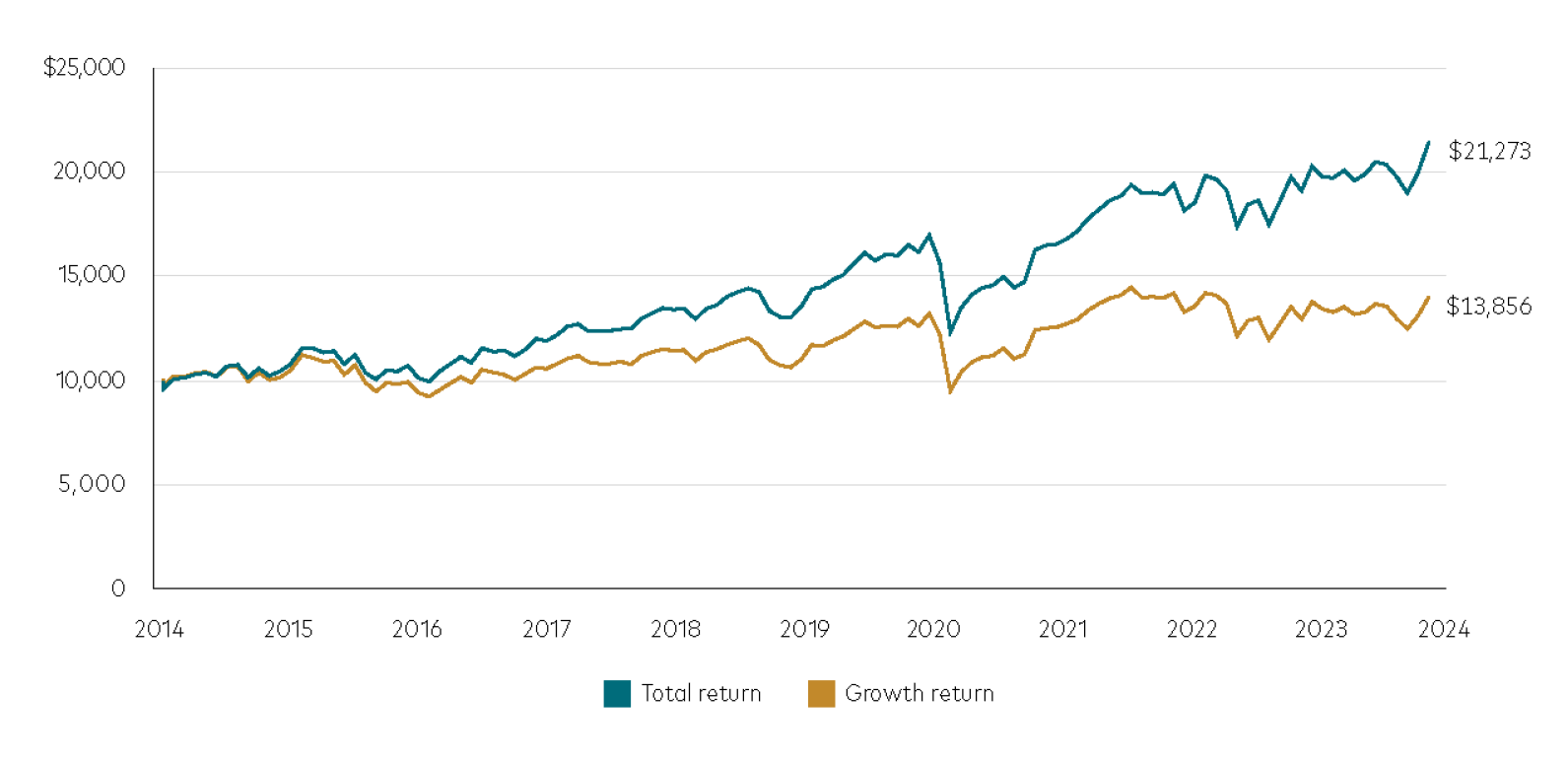

Let’s take a hypothetical investor who invested $10,000 into VAS on 1 January 2014, purchasing 147 units (based on VAS’s $67.83 net asset value per unit at the time).

The chart below compares the growth return and the total return from that investment over the 10-year period between 1 January 2014 and 31 December 2023.

The growth return represents the base return from their VAS holding, while the total return includes all the distributions paid by VAS and assumes they were reinvested over the same time period to purchase more VAS units.

10-year investment in VAS with and without reinvestment

Sources: Calculations are based on a $10,000 investment into the Share Index ETF from 1 January 2014 to 31 December 2023.

Notes: Returns assume that an investor purchased shares at Net Asset Value (NAV) and does not reflect the transaction costs imposed on the creation and redemptions of ETF units, brokerage or the bid ask spread that investors pay to buy and sell ETF securities on the Australian Securities Exchange.

Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance.

The growth return over the measured period was 38% and would have resulted in the $10,000 initial investment increasing to $13,856 based on VAS’s net asset value per unit of $94.42 at 31 December last year. The hypothetical investor also would have received $4,957 in income distributions over the 10 years.

By comparison, if the investor had chosen to reinvest all their income distributions into additional VAS units, they would have achieved a total return of 113% and their end investment balance at 31 December last year would have grown to $21,273.

On a dollar basis, by including the cash dividends paid out, there would have been an overall difference of about $2,460, or 13.1%.

But the bigger benefit from reinvesting is that the number of ETF units held continued to compound over time.

By using their income distributions to buy additional VAS units, the hypothetical investor’s unitholding would have increased by 78 from the original 147 units to 225 units.

As such, they would have received compounding investment returns over the 10-year period based on the gradual increase in the number of VAS units they held.

The investor also would have saved a significant amount in brokerage fees on the additional ETFs purchased through reinvesting.

This hypothetical comparison demonstrates that investors who consistently reinvest their income distributions will likely achieve higher investment returns over the longer term compared to those who choose to take their distributions as cash.

Investors holding ETFs through a Personal Investor Account can simply login and update their income preference to ‘reinvest’ to have distributions automatically reinvested.

Important Information

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) (“Vanguard”) is the issuer of the Vanguard® Australian ETFs. Vanguard ETFs will only be issued to Authorised Participants. That is, persons who have entered into an Authorised Participant Agreement with Vanguard (“Eligible Investors”). Retail investors can transact in Vanguard ETFs through Vanguard Personal Investor, a stockbroker or financial adviser on the secondary market.

We have not taken your objectives, financial situation or needs into account when preparing this publication so it may not be applicable to the particular situation you are considering. You should consider your objectives, financial situation or needs, and the disclosure documents for Vanguard’s products before making any investment decision. Before you make any financial decision regarding Vanguard’s products you should seek professional advice from a suitably qualified adviser. The Target Market Determination (TMD) for Vanguard’s ETFs include a description of who the ETF is appropriate for. You can access our IDPS Guide, PDSs Prospectus and TMD at vanguard.com.au or by calling 1300 655 101.

Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance.

An investment in Exchange Traded Funds (ETFs) is subject to investment and other known and unknown risks, some of which are beyond the control of Vanguard, including possible delays in repayment and loss of income and principal invested. Please see the risks section of the Product Disclosure Statement (“PDS”) for the Vanguard Australian Shares Index ETF for further details. Neither Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) nor its related entities, directors or officers give any guarantee as to the success Vanguard Australian Shares Index ETF, amount or timing of distributions, capital growth or taxation consequences of investing in the Vanguard Australian Shares Index ETF.

This publication was prepared in good faith and we accept no liability for any errors or omissions.

© 2024 Vanguard Investments Australia Ltd. All rights reserved.

Tony Kaye, Senior Personal Finance Writer

March 2024

vanguard.com.au